This is part of the Forward Guidance newsletter. To read the full editions, Subscribe.

Since the coronavirus shut down global economies in 2020, measuring where we are in the business cycle has become a very difficult feat.

A typical business cycle looks like this, and historically, it has been fairly easy to get a general idea of where we stand by comparing interest rates and monetary policy:

However, everything has turned somewhat upside down in recent years, leaving many economists scratching their heads.

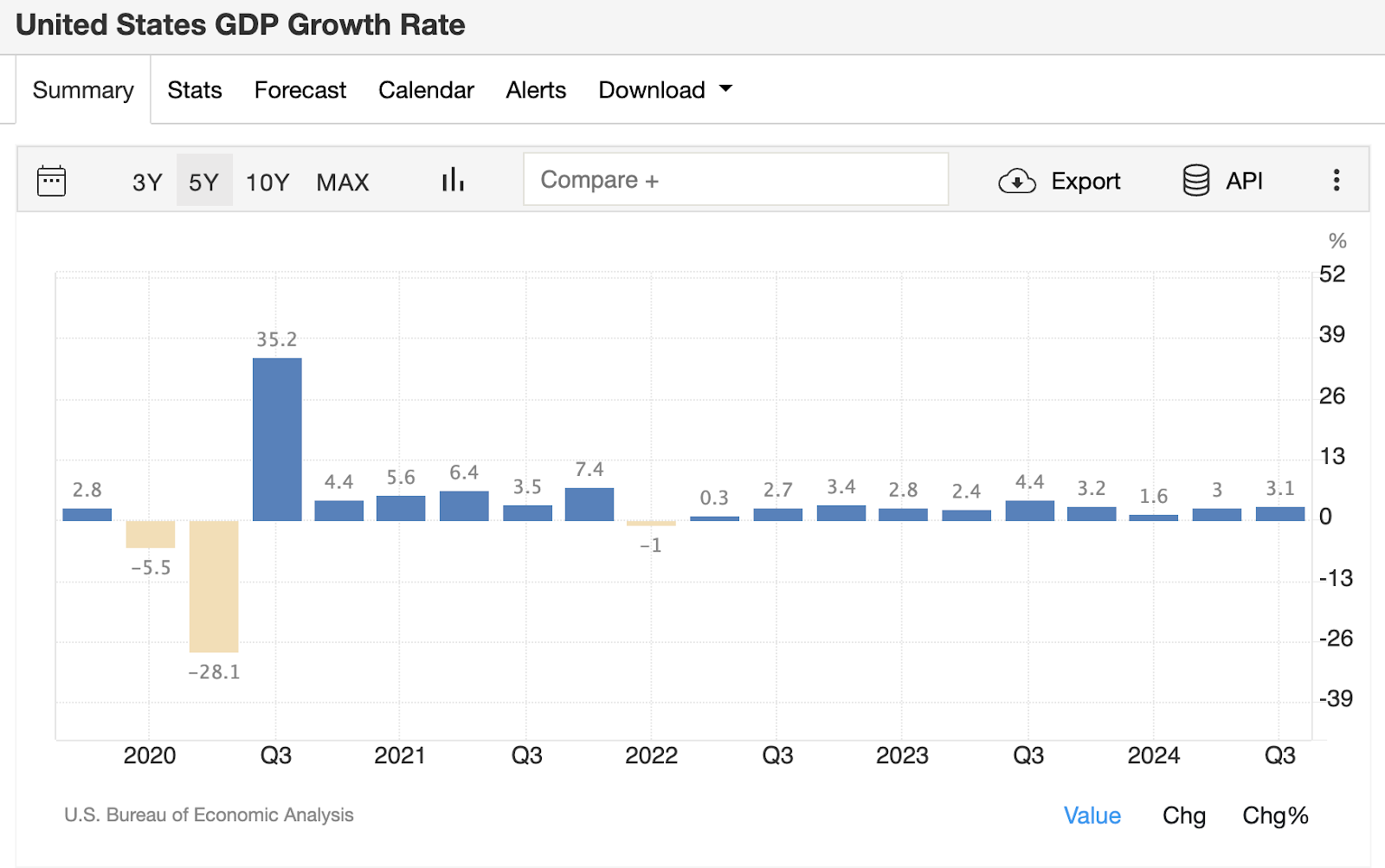

For example, in 2022 we saw negative real GDP prints (initially at two but then revised to one):

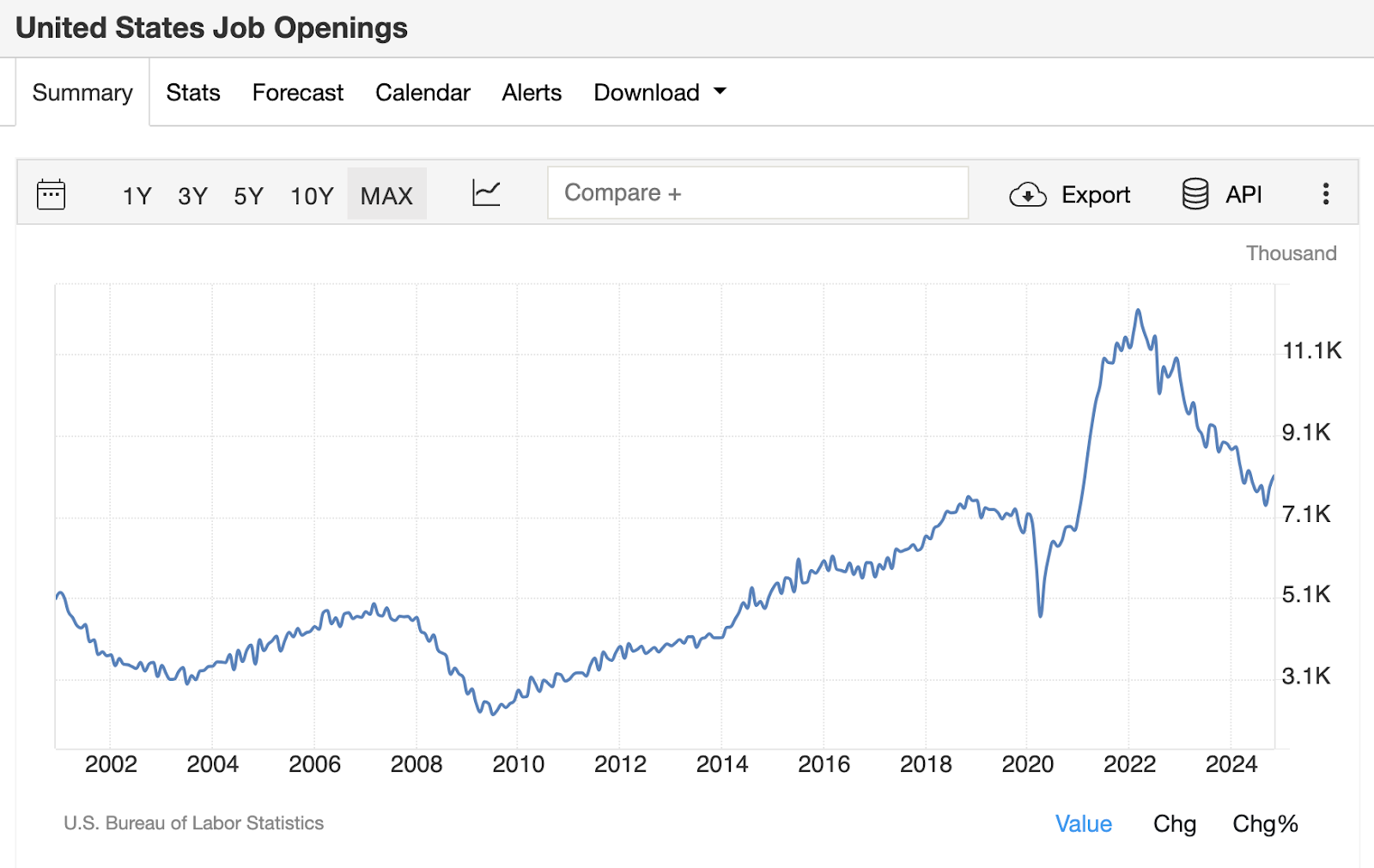

However, during that same period, we experienced one of the hottest job markets we have ever seen, according to JOLTS data.

It's hard to believe a recession is happening with a job market this strong:

Since 2022, we have seen a major cycle of Fed rate hikes that has not somehow pushed the economy into recession when viewed on an aggregate basis. Stocks hit new highs every day, the labor market slowed but remained resilient, and GDP growth moved forward.

However, during that same period, if you focus on the manufacturing and goods sector and put the services economy aside, it looks like we just went through a manufacturing recession.

ISM Manufacturing PMIs have been in contraction territory for two years now:

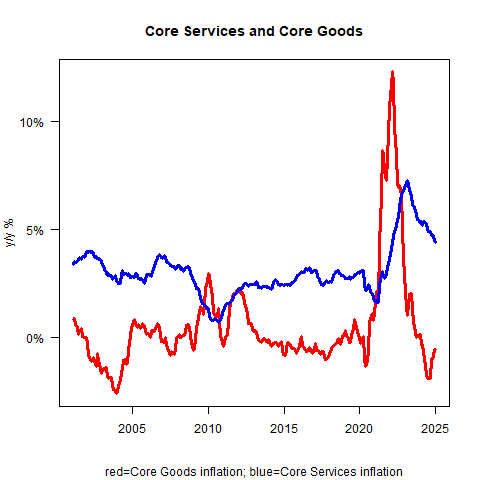

During that period, we saw a significant decline in inflation which led to an outright contraction in the goods sector of the economy:

Moving forward to today, we have seen the Fed cut interest rates to calm concerns about the labor market and continue to attempt a soft landing on the economy as we move into a new business cycle without a recession.

We are now seeing key indicators that the manufacturing sector may be emerging from the recession and heading towards a new recovery.

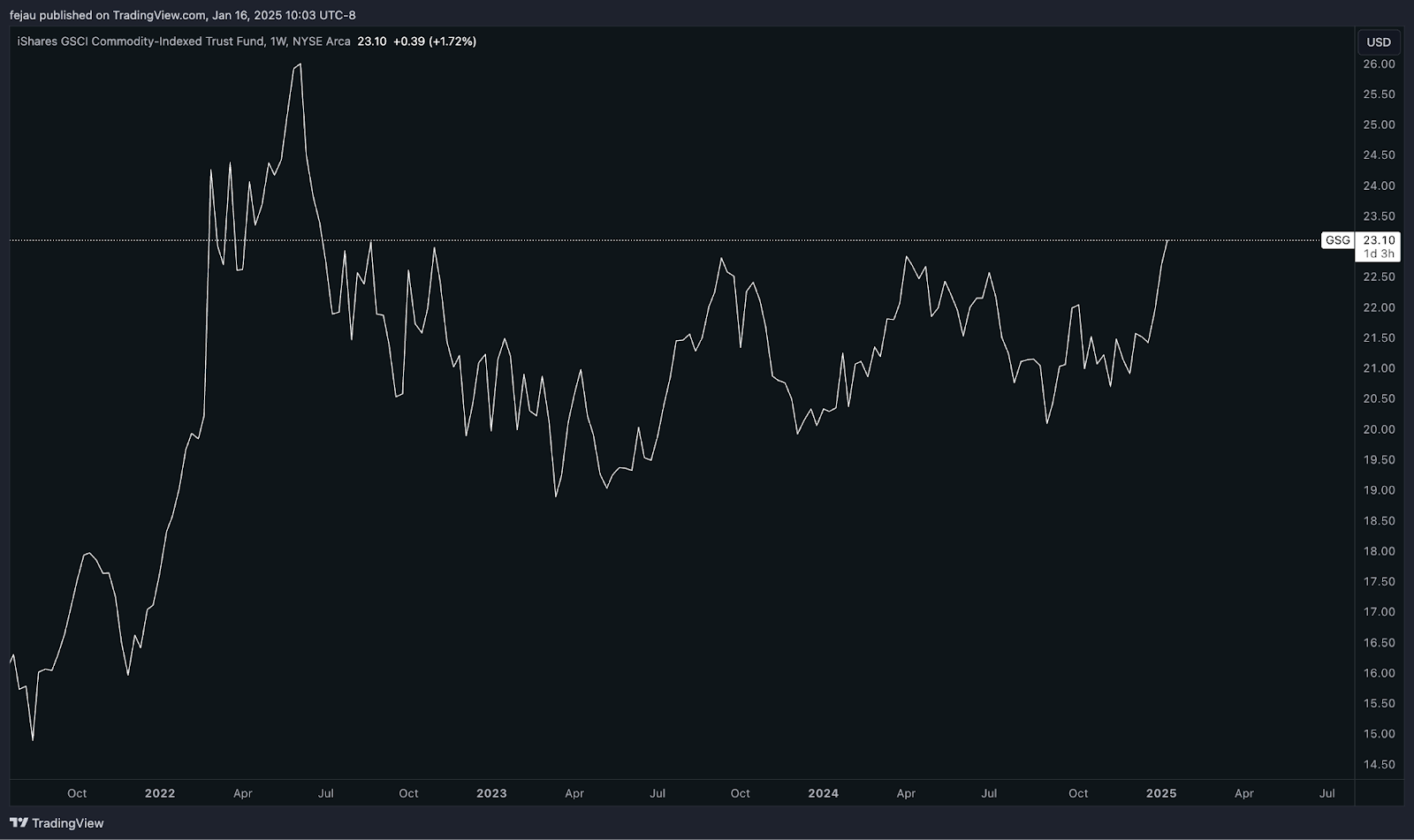

We are starting to see commodities start to rise after two years of consolidation, indicating a pick-up in economic growth:

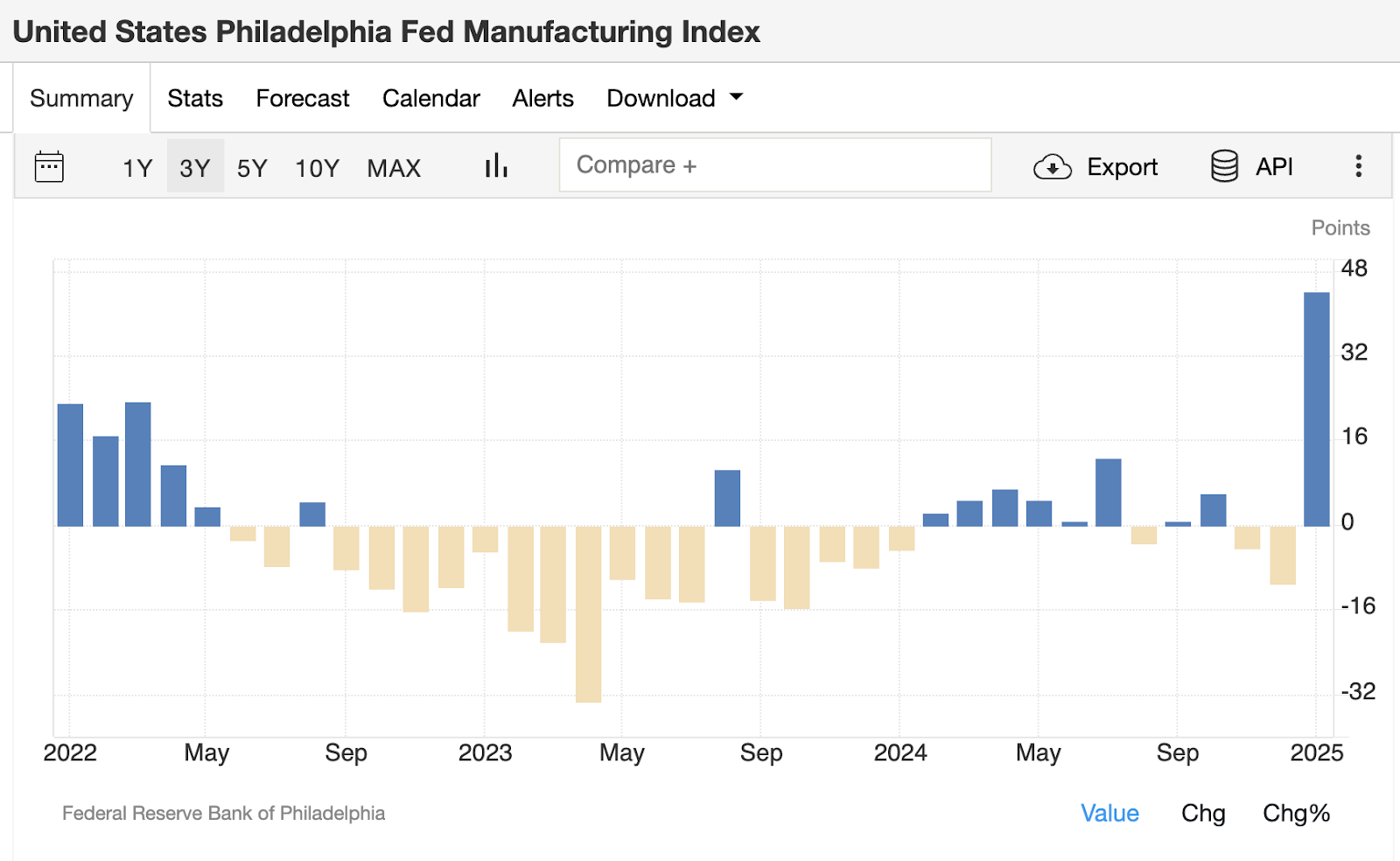

It appears that new orders from the ISM are starting to appear, as well as the Philadelphia Fed Manufacturing Index:

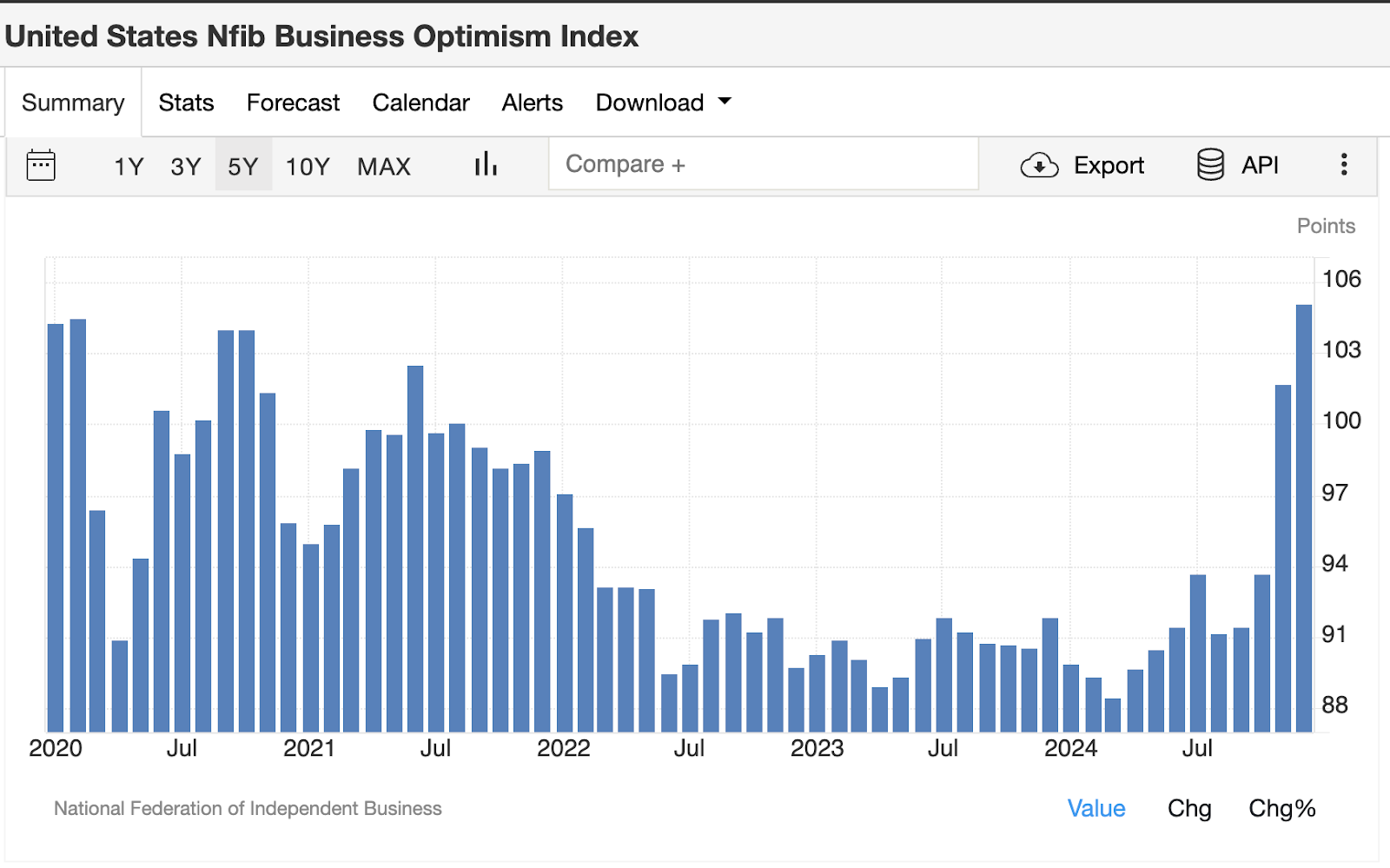

According to survey data, much of this appears to be driven by optimism from the business sector since then election:

So where does this graphing journey lead us?

I think it's safe to say we're not late in the course. It increasingly looks as if we are actually in the early stages of a new business cycle that has avoided recession due to massive fiscal stimulus and deficits over the past two years.

Start your day with the best cryptocurrency insights from David Kanellis and Katherine Ross. Subscribe to the Empire Newsletter.

Explore the growing intersection between cryptocurrencies, macroeconomics, politics, and finance with Ben Strack, Casey Wagner, and Felix Goffin. Subscribe to the Forward Way Newsletter.

Get alpha straight to your inbox with 0xResearch Newsletter — Market highlights, charts, trading ideas, management updates, and more.

The Lightspeed Newsletter has everything Solana, in your inbox every day. Subscribe to Solana Daily News By Jack Kopenick and Jeff Albus.

Source link