This is part of the Forward Guidance newsletter. To read the full editions, Subscribe.

For those who don't know, I'm Canadian. However, I spent almost every hour of the day thinking about macroeconomics from a US perspective. In the world of markets, the United States is the center and everything else is secondary.

Thinking about the two worlds I live in makes for an interesting little story about why the Fed continues to stop and start its approach to monetary policy regarding the economy.

The unemployment rate in Canada has reached its highest level at 6.8%, and looks set to rise to higher levels, while the unemployment rate in the United States appears to be stable. Yes, both economies have been affected by increased labor supply due to immigration, but the Canadian labor market is worse across the board.

Canada has managed to bring inflation back to 2% on an annual basis, while the United States has remained stubbornly above target.

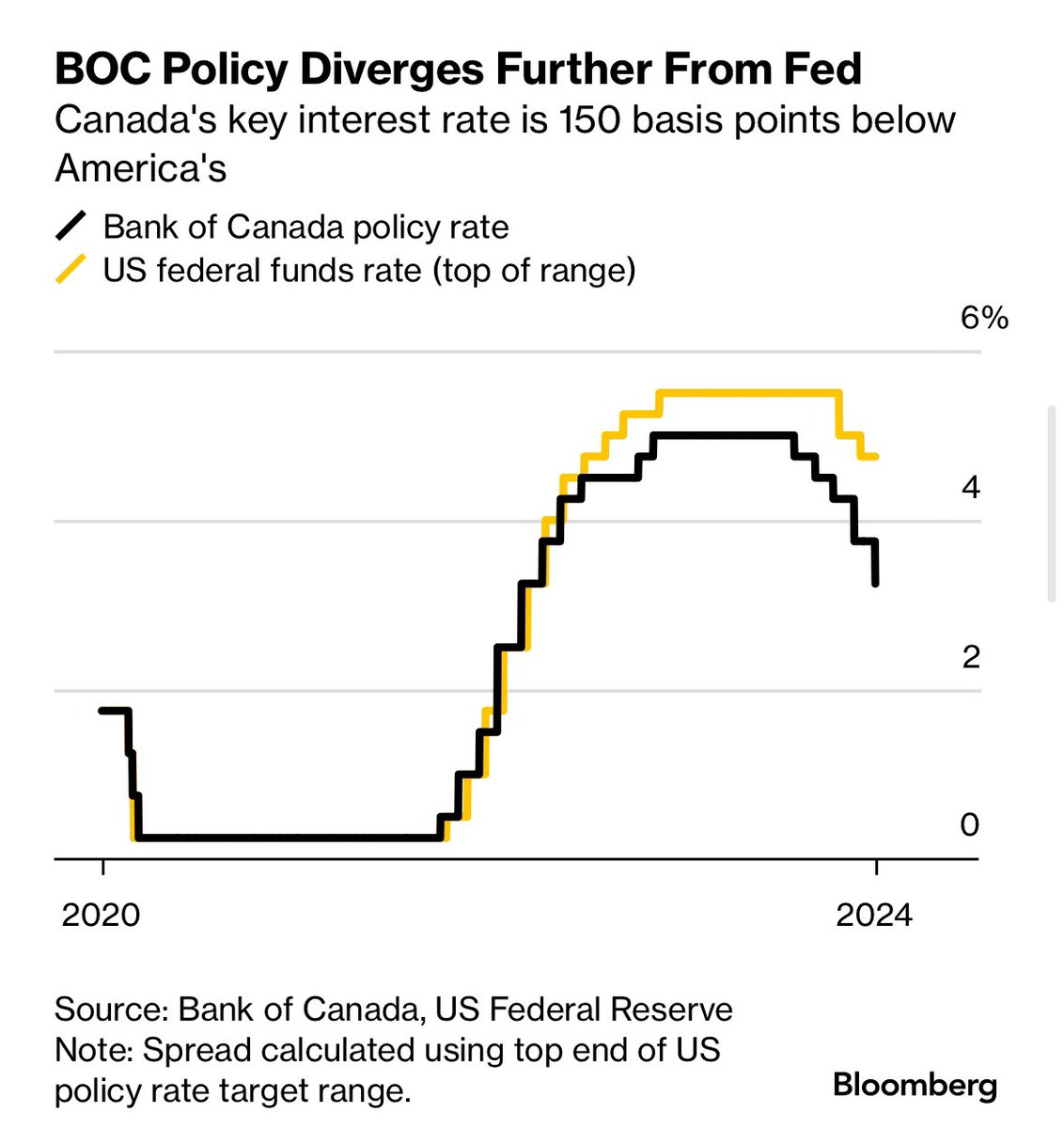

The Bank of Canada surprised markets this week by cutting interest rates by another 50 basis points versus the recent 25 basis point cuts it had been making. The US is expected to cut interest rates again next week before pausing for a while as the economy continues to surge.

So what gives? What drives this discrepancy between two similar economies that trade closely?

It is simply that the financial system in the United States is less sensitive to changes in short-term interest rates than the financial system in Canada. Here are two examples:

Companies

US companies have access to the world's largest debt markets and can issue fixed-rate bonds with low spreads, while Canadian companies (as is typical in non-US countries) are more inclined to issue floating-rate debt, which changes at Immediately with changes in the central bank policy rate.

Captivity

In the US, homeowners can continue to get a fixed-rate mortgage for 30 years, and as long as they don't move, the Fed can raise interest rates to 50% and it won't affect them. The rate they lock in is the rate for the entire mortgage. Given the number of households that refinanced their mortgages at the lows of Covid (less than 3%), as long as they don't move, they are unaffected by interest rate increases. This is very different in Canada and most other countries, where the rate resets every five years, even on a 25-year fixed rate mortgage. So, even if homeowners stay put, they will eventually be affected by the price increase.

These two examples illustrate why the Fed has so much trouble getting into a consistent policy path—its main instrument cannot influence large sectors of the economy as it does in other countries. Here we are instead, with an increasing fragmentation of economies between the United States and everyone else. Oh, the beautiful American exceptionalism.

Start your day with the best cryptocurrency insights from David Kanellis and Katherine Ross. Subscribe to the Empire Newsletter.

Explore the growing intersection between cryptocurrencies, macroeconomics, politics, and finance with Ben Strack, Casey Wagner, and Felix Goffin. Subscribe to the Forward Way Newsletter.

Get alpha straight to your inbox with 0xResearch Newsletter - Market highlights, charts, trade ideas, management updates, and more.

The Lightspeed Newsletter has everything Solana, in your inbox every day. Subscribe to Solana Daily News By Jack Kopenick and Jeff Albus.

Source link